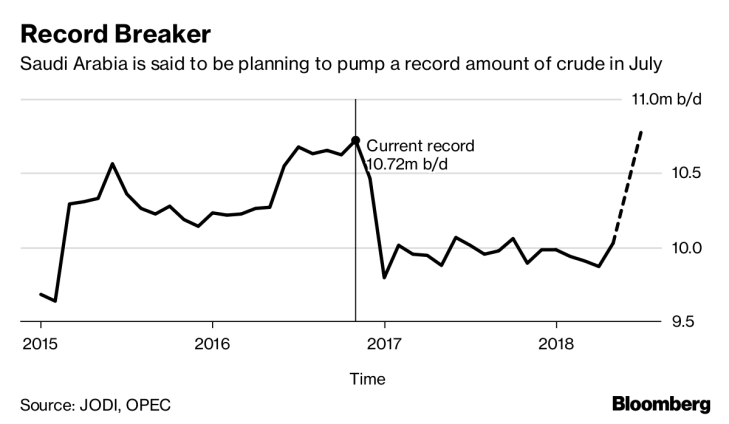

Two major oil producers, Russia and Saudi Arabia have decided that instead of co-operating on production amounts, they will fight it out, testing each other’s economic stamina. Mr. Putin may think himself a tough guy, but during the hideous world recession in 2008, when oil prices dropped by almost 60 percent, Russia came close to bankruptcy. Saudi Arabia owns almost 25 percent of the world’s oil reserves. As the demand for oil is usually quite stable, even a five percent increase in production can crater the market price of crude. The effects of a production increase look all the greater with oil demand actually falling thanks to the coronavirus’s impact on world trade, which is slumping as much s fifty percent, at least in the short term.

A detailed overview of the Saudi oil increase and Russia’s objections can be found here : https://www.ft.com/content/59dcba56-61a2-11ea-b3f3-fe4680ea68b5

So much for background. My intention in this column is to parse out some of the effects the Saudis’ oil production increase will likely have on the American economy.

First : prices of gasoline are declining at the pump by about 25 percent. Immediately that means that the gas tax increase passed last week by the Massachusetts House loses, if enacted, 25 percent of its anticipated income. Or, the legislation had a secondary purpose : to discourage people from driving wherever possible, That purpose now looks on hold.

Second : the present price of crude in the market is about $ 27.88 per barrel. At that price most American producers cannot produce. If the price cut lasts, US producers will come under major financial stress. Most are highly leveraged — operating on borrowed money — which they cannot pay back if they can’t sell crude at a price above their cost. (This has happened before. In the mid-1980s the price of crude, jacked way way up during the 1970s because of Saudi production cuts, fell from $ 60 per barrel to as low as $ 5.00; many exploration and extraction firms went belly-up.) Probably the Saudi production spurt won’t last as long as the 1980s production cuts — the Saudis aren’t immune to an oil price recession — but if it goes on for even six months, it will impact many firms that are already experiencing a decline in demand because of COVD-19.

Third : the success of present clean energy programs depends upon being able to compete on price with the cost of fossil fuels. A 25 percent decrease in gasoline, oil and natural gas costs sets back ,the process of conversion to “clean energy” systems.

Oil is not only the major source of energy. Its also one of the world’s most widespread investments. A sustained 25 percent decline in the price of crude forces investors to hedge their contract commitments, which means borrowing money — money backed ultimately by US Treasury bonds at a time when huge demand for safe investments has driven the interest rate ion “Treasuries” below one percent, almost into negative territory. A negative interest rate is, in effect, a tax. The 2018 tax cut legislation has put enormous sums of corporate and investment money on the sidelines, parked in money market accounts and “Treasuries,” money that, in order to remain parked safely, will, if interest rates go negative, incur an interest penalty in place of a money return.

Fourth : the current US budget deficit is running a TRILLION dollars yearly. That trillion dollars is backed by Treasury bonds and notes which the Treasury buys from investors, whose own trillions of parked money bought these bonds to begin with. But with both investors and the Treasury buying Treasury bonds, the seller vs. buyer equilibrium tilts radically in favor of the seller, who sells for a price, not on the basis of his coupon rate, which he no longer owns. That is why interest rates have fallen almost to zero. And why with the Saudi oil production increase can only fall further, as investors who would ordinarily buy oil forward contracts decide to avoid the market and buy Treasury notes instead.

Fifth : the decline in economic activity due to the virus, linked to the Saudis’ decision to slash oil prices via over-production, threatens to turn our economy downward, into recession, at a time when there is very little flexibility available, in either bond markets or money availability — thanks to huge operating deficits — to stimulate economic activity, which activity is already limited by the inadequacy of wages paid to at lest half of all American workers. American workers have no money to spare, nothing to spend on discretionary products, and in the present coronavirus situation, less inclination to spend it anyway. A recession in these circumstances would be painful, very painful.

—- Mike Freedberg / Here and Sphere